Last time, the RSI 30/70 strategy died at gate 2 — fees ate it alive before we even got to the interesting questions. This strategy is different. It’s the first one to make it deep into the 7-Gate Protocol: five symbols, sixteen parameter sets, and a full out-of-sample split.

It survived more gates than anything we’ve tested. It still didn’t survive all of them. Here’s the complete autopsy — including exactly where it works and where it dies.

The Exact Rules

- Timeframe: 4H candles

- Trend filter: EMA(100) — longs only above it, shorts only below it

- Entry: price pulls back and touches the daily VWAP, then closes back in the trend direction

- Stop loss: fixed at entry ± 2.0 × ATR(14) — never trailed

- Exit: close crossing back through the EMA(100) (trend over), or the stop

- Fees: 0.06% per side, intrabar stop fills

- Data: 2 years (July 2024 – July 2026), Binance public data

One counterintuitive detail from our earlier testing: a trailing stop destroys this strategy (PF 0.76). Pullback entries get shaken out by noise. The fixed stop is not a preference — it’s the difference between profit and ruin.

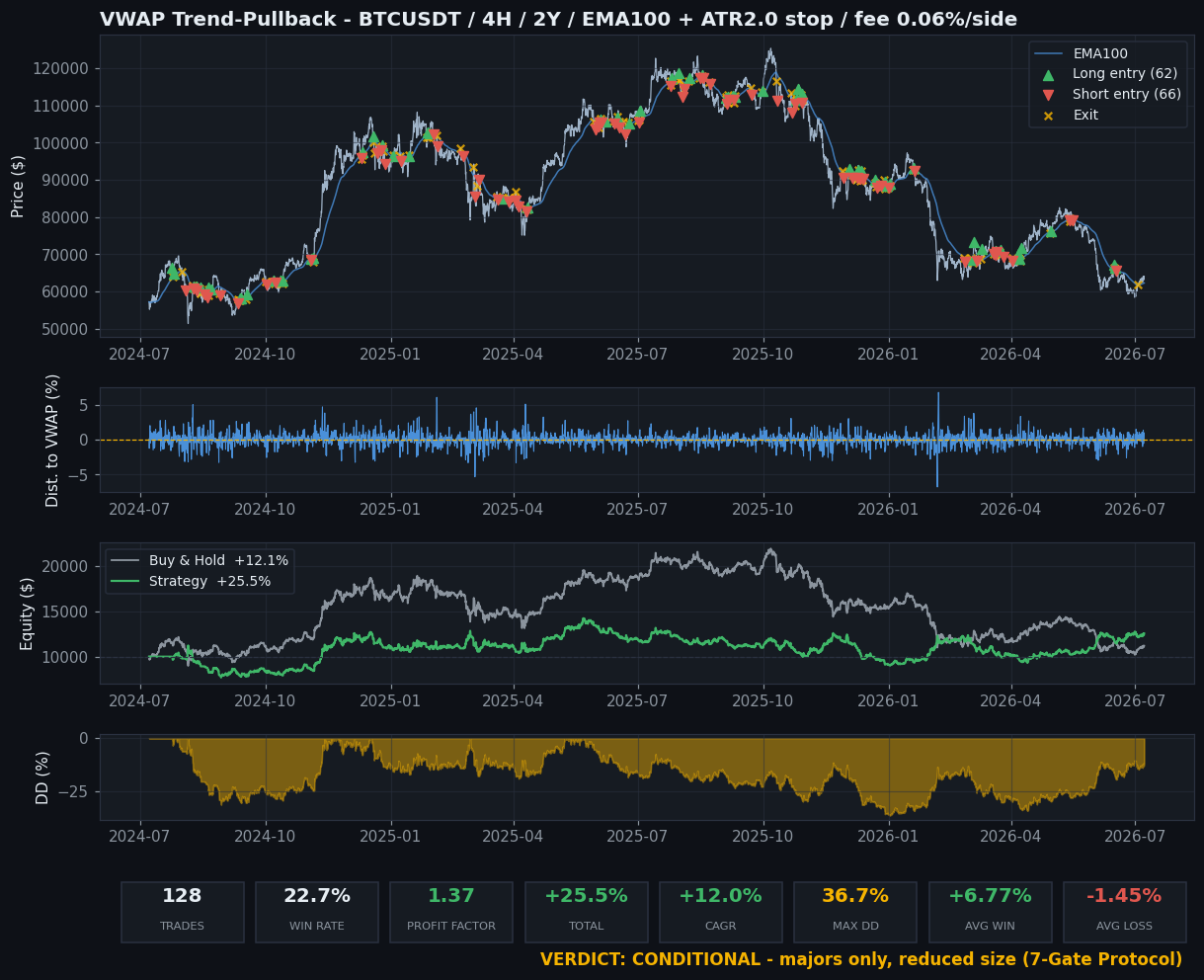

The Baseline: BTC, 4H

Look at that win rate: 22.7%. Three losses out of four trades — and it still made +25.5%, double Buy & Hold. This is the exact mirror image of the RSI lesson: average win +6.77%, average loss −1.45%. Win rate is a vanity metric. Payoff asymmetry is the business model.

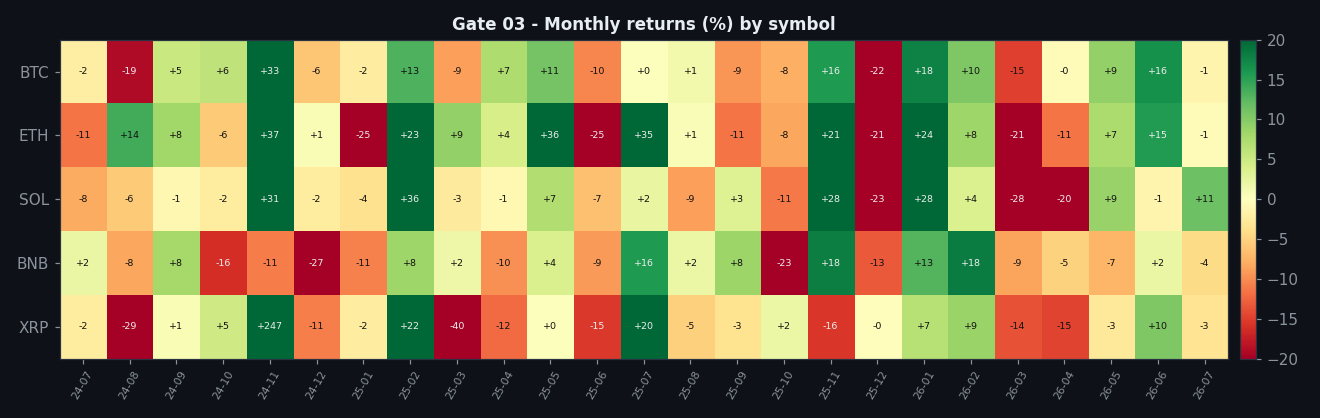

Gate 03 — Monthly Consistency

Not pretty, not terrible. Long flat-to-red stretches punctuated by big green months — the classic trend-following profile. You don’t get paid monthly; you get paid when trends happen.

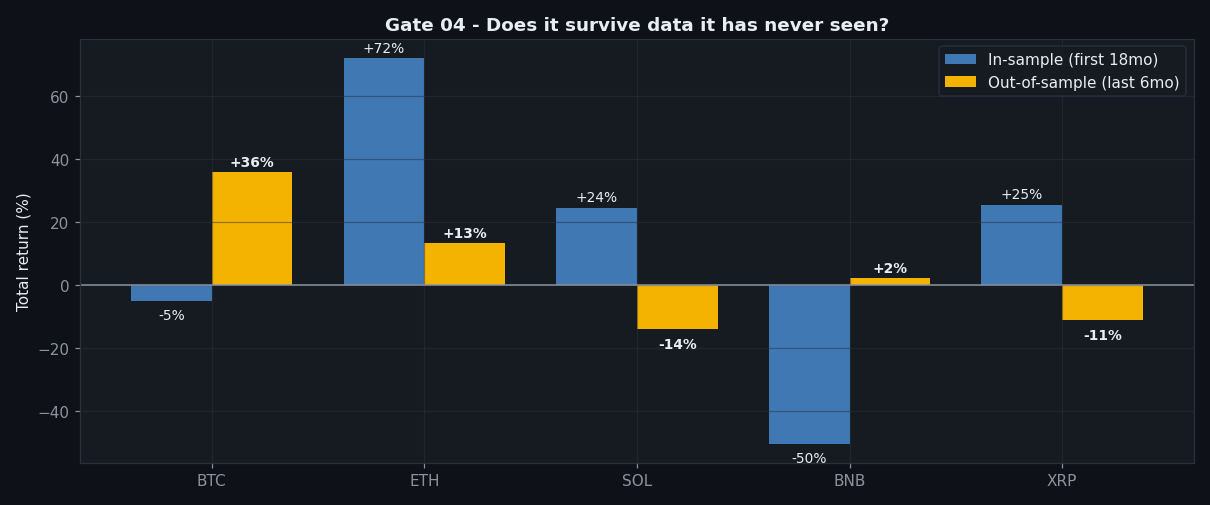

Gate 04 — Out-of-Sample

We split the data: first 18 months in-sample, last 6 months untouched. 3 of 5 symbols stayed positive out-of-sample. BTC actually got better (PF 2.46 out-of-sample). SOL and XRP flipped negative. Partial pass — the edge doesn’t evaporate on unseen data, but it’s not universal either.

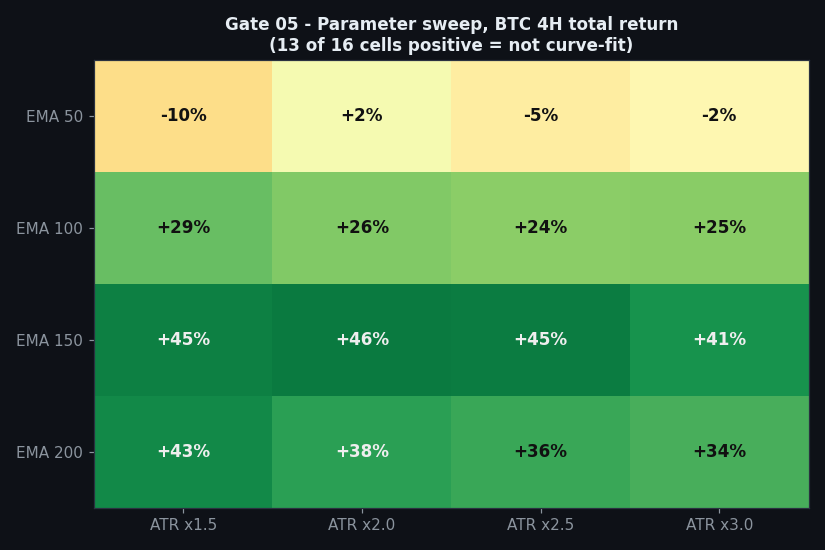

Gate 05 — Parameter Robustness

Sixteen combinations of EMA length (50–200) and ATR stop multiple (1.5–3.0): 13 of 16 positive. This is what a real edge looks like — it degrades gracefully when you wiggle the knobs. A curve-fit strategy shows one green cell in a sea of red.

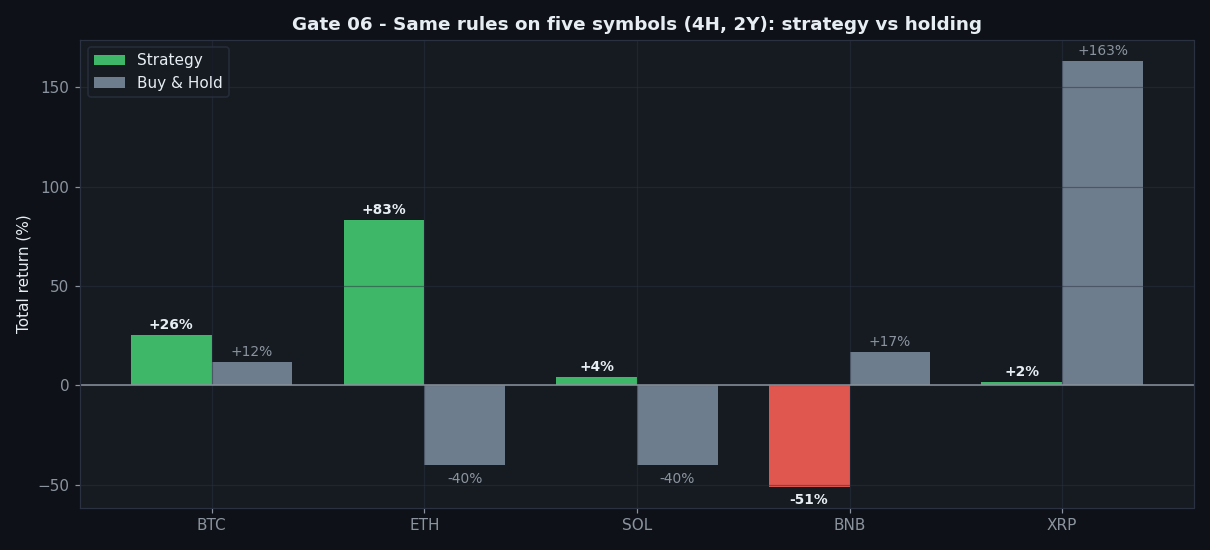

Gate 06 — Five Symbols, Same Rules

| Symbol | Trades | PF | Total return | Max DD | Buy & Hold | Verdict |

|---|---|---|---|---|---|---|

| BTC | 128 | 1.37 | +25.5% | 36.7% | +12.1% | beats holding |

| ETH | 128 | 1.51 | +83.3% | 41.8% | −39.8% | crushes holding |

| SOL | 133 | 1.15 | +4.2% | 51.1% | −40.2% | beats holding |

| BNB | 165 | 0.80 | −50.8% | 60.6% | +16.8% | fails |

| XRP | 148 | 1.68 | +1.5% | 75.9% | +163.2% | loses to holding |

This is why gate 06 exists. Test on BTC alone and you’d call it a winner. Test on BNB and you’d call it garbage. Both would be wrong: the edge is real on majors and absent elsewhere. Anyone selling you a strategy that “works on everything” hasn’t run this test.

The Verdict: CONDITIONAL

Adding up the gates:

- Gate 01 sanity — pass (signals on closed bars, no lookahead)

- Gate 02 friction — pass (profitable after 0.06%/side; where RSI died)

- Gate 03 yearly/monthly — partial (trend-dependent, long flat stretches)

- Gate 04 out-of-sample — partial (3/5 positive)

- Gate 05 robustness — pass (13/16 cells)

- Gate 06 multi-market — partial (majors yes, BNB fatal)

- Gate 07 vs B&H — partial (3/5)

Our verdict stamp says CONDITIONAL, and now the conditions are precise:

Majors only (BTC/ETH). Reduced position size — the 37–42% drawdowns are real. As a portfolio component, not a standalone system. Traded outside those conditions, expect the BNB outcome.

That nuance is the whole point of this site. A YouTube title would say “this VWAP strategy made 83% on ETH!” A different YouTube title would say “I tested VWAP and lost 50%!” Both are technically true. Neither is the truth.

FAQ

Why does it fail on BNB?

BNB spent much of the window in choppy, range-bound conditions where trend filters generate false regime signals. The strategy needs trends; BNB didn’t provide them.

Would a different VWAP (weekly, anchored) help?

In our earlier tests, weekly VWAP performed worse as a touch level. Volume-profile POC levels also degraded results — daily VWAP carried all the edge.

What about the low win rate — can I handle 3 losses out of 4?

That’s the real question. Statistically it works; psychologically most people abandon it during the losing streaks. That’s a you-parameter, not a strategy parameter.

Can I replicate this?

Yes — the rules above are complete, data is public Binance OHLCV, fees 0.06%/side. Every number in this article falls out of those inputs.

Disclaimer: This is educational research, not financial advice. Past performance does not guarantee future results. Never trade money you cannot afford to lose.

Leave a Reply